The NJPP's reports are highly misleading because pensions are just one part of an big enchilada of benefits and privileges that NJ retired teachers get.

- NJ teachers get Social Security, not all teachers do.

- NJ teacher pensions are based on salaries that are higher than what teachers get in most other states.

- NJ teachers get post-retirement healthcare, not all retired teachers do.

- NJ teacher pensions are untaxed.

Additionally, the NJPP exaggerates the monetary value of COLAs in other states, where often COLAs are significantly less than inflation.

The NJPP pension reports came out in 2014 ("New Jersey has Modest Public Pension Benefits") and 2017, ("New Jersey Pensions Rank Among the Least Generous in the Nation") and have overlapping data and arguments. They were written by Stephen Herzenberg, who is not a full-time NJPP staffer, but an activist who normally concentrates on Pennsylvania. As usual with NJPP authors, Herzenberg did not acknowledge in his reports that the NJPP is funded by the New Jersey Education Association.

As it does in many other contexts, the NJPP is inconsistent in its comparison points in order to make arguments that support its funders' needs and/or ideological beliefs, in this case, the belief to be supported is that NJ teachers are undercompensated.

- The pension reports use interstate comparisons between public employee pensions in New Jersey versus public employee pensions in other states to say that NJ's pensions are ungenerous. There is no attempt to compare NJ public employee pensions with private sector pensions (which are usually not DB plans).

- The teacher salary reports use intrastate salary comparisons between NJ teachers versus other NJ workers with bachelors degrees. There is no attempt to compare NJ teacher salaries with salaries of teachers in other states (which are lower all but three states).

The NJPP also uses divergent interstate comparisons of pension generosity.

- In comparing pensions based on what percentage of final salary a retiree receives, Herzenberg and the NJPP compare New Jersey to all other states and non-teacher pension plans.

- In comparing pensions on the dollar amount of the pension, Herzenberg and the NJPP compare New Jersey to only seven other high-cost states, Vermont, Alaska, Maryland, New York, Connecticut, California, and Massachusetts.

Despite the many flaws of the analyses (which I'll explore below), the claim that NJ pensions are modest and ungenerous have caught on in the teacher union-intellectual universe and op-ed pages. Brian Rock, writing in the NJ Spotlight in March 2019, uncritically believed the reports saying:

In December 2017, New Jersey Policy Perspective released a brief on pensions that compared New Jersey’s system with those in other states, and it found that the Normal Cost of TPAF was average — 35th out of the 69 pension systems they compared it to. Meanwhile, New Jersey’s other main pension fund, the Public Employees’ Retirement System (PERS), was even cheaper. Its Normal Cost is equivalent to 2.4 percent of salary, the 13th lowest rate of these 69 pension systems.

The answer to our problem is not to further reform the pension system. Public employees have already seen their contributions increase to 7.5 percent of their salary. Meanwhile, the headline of NJPP’s brief was, “New Jersey Public Pensions Rank Among Least Generous in the Nation,” so it’s not like there’s any room left to cut benefits.Mark Weber (aka Jersey Jazzman) also uncritically cited the reports in his 2019 and 2020 reports claiming that NJ's teachers were underpaid.

In 2014, an NJPP analysis found: “…New Jersey ranks 95th in pension generosity among the country’s 100 largest plans.” 40 The ranking was based on the fact the New Jersey pensions have relatively low multipliers – the percentage by which the state calculates pension payments per years of service – as well as no protection for inflation and higher employee contributions than two-thirds of the other plans surveyed. In addition, a 2017 survey of teacher pensions across states found New Jersey’s vesting requirement of 10 years to be among the highest in the nation

The NJPP's Claims are Based on Three Factors Only

The Herzenberg/NJPP claim is a judgment only of pensions after the post-Chapter 78 reforms, which have not yet begun to effect the majority of teachers and retirees since most NJ teachers and retirees worked before 2011.It is solely Tier 5 that the New Jersey Policy Perspective/Herzenberg evaluate as a penurious pension plan, based on these three factors.

Quoting from the 2014 report:

Quoting from the 2014 report:

- New Jersey retirees have no automatic protection against inflation. While 69 of the 100 largest plans offer retirees some inflation protection, cost-of-living adjustments for New Jersey retirees were suspended indefinitely by the 2011 legislative pension reforms.

- New Jersey uses a very low multiplier. The percentage by which New Jersey calculates state pensions per year of service – known as the multiplier – is among the lowest nationally, at 1.67 percent. This means pensions benefits equal 1.67 percent of final salary multiplied by the number of years of service; 1.67 percent is a lower multiplier than all but 21 of the 100 plans. New Jersey lowered the multiplier from 1.81 percent in 2011.

- New Jersey employees pay more into the system than those in most other systems. New Jersey public employees contribute 6.93 percent of their salaries to their own pensions, more than 55 other plans in the top 100. By 2018, the employee contribution level for New Jersey pensions will rise to 7.5 percent, which is more than employees contribute today in about two-thirds of the top 100 plans.

Social Security

There are fifteen states where no teachers receive Social Security and another three states where some teachers don't receive Social Security.

States where no teachers are eligible for Social Security are Alaska, California, Colorado, Connecticut, Illinois, Louisiana, Maine, Massachusetts, Missouri, Nevada, Ohio, and Texas.

The NJPP analysis emphasizes that NJ's post-2011 pension multiplier is 1.67% of final salary times years employed (n/60), versus the more common 1.81% (n/55), but applied to NJ's high teacher salaries, NJ teacher pensions are quite high in national comparison.

States where no teachers are eligible for Social Security are Alaska, California, Colorado, Connecticut, Illinois, Louisiana, Maine, Massachusetts, Missouri, Nevada, Ohio, and Texas.

Some teachers in Georgia, Kentucky, and Rhode Island are ineligible.

All-in, 40% of American teachers don't get Social Security.

Recall that Steven Herzenberg/NJPP directly compares NJ's pensions to other high cost states. Of the high cost states Herzenberg/NJPP cites that have better pensions, only New York gives teachers Social Security. Connecticut, California, and Massachusetts do NOT.

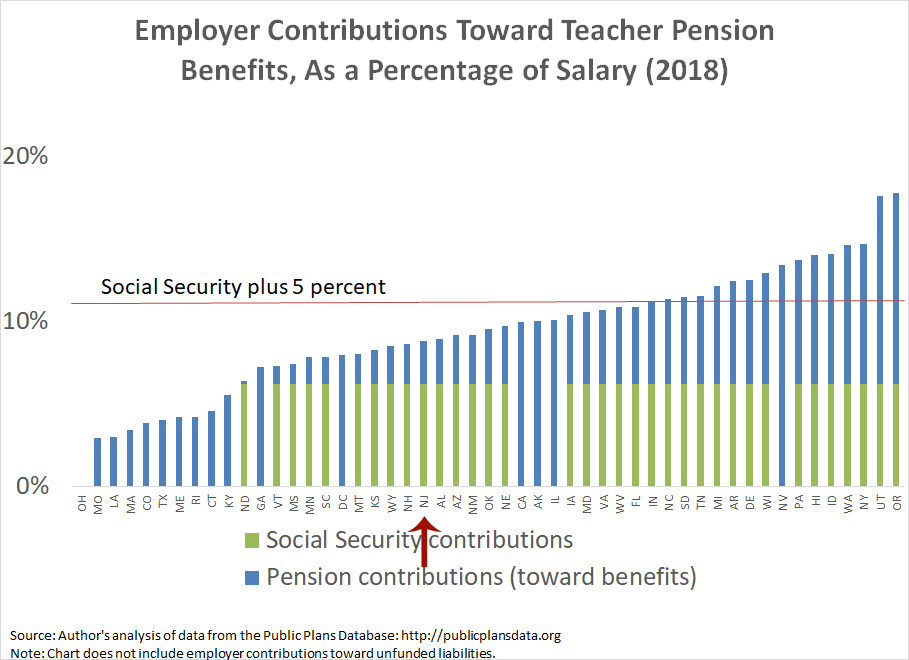

By contrast, all New Jersey teachers receive Social Security, so if you factor in Social Security costs alone, New Jersey's pension costs per teacher are solidly in the middle of the country (see graph below).

Recall that Steven Herzenberg/NJPP directly compares NJ's pensions to other high cost states. Of the high cost states Herzenberg/NJPP cites that have better pensions, only New York gives teachers Social Security. Connecticut, California, and Massachusetts do NOT.

|

| Add caption |

By contrast, all New Jersey teachers receive Social Security, so if you factor in Social Security costs alone, New Jersey's pension costs per teacher are solidly in the middle of the country (see graph below).

According to Chad Aldeman, NJ's pension plus Social Security employer-side benefit costs are the 30th highest as a percentage of salary.

In New Jersey, teachers Social Security is paid by the state and is a large expense: $785.5 million for FY2020, or 5% of NJ's state government's education spending, so not a trivial amount.

Pensions are a Lower Percentage of Salaries Than in Most other States, But NJ Salaries are Higher

Both Herzenberg/NJPP and Chad Aldeman actually use the same basis for comparison. Herzenberg and the NJPP use pensions as a percentage of salary, and Aldeman uses pensions+Social Security as a percentage of salary, but if you actually look at what NJ's salaries are, NJ's teacher pensions are quite high in dollars per year of employment.

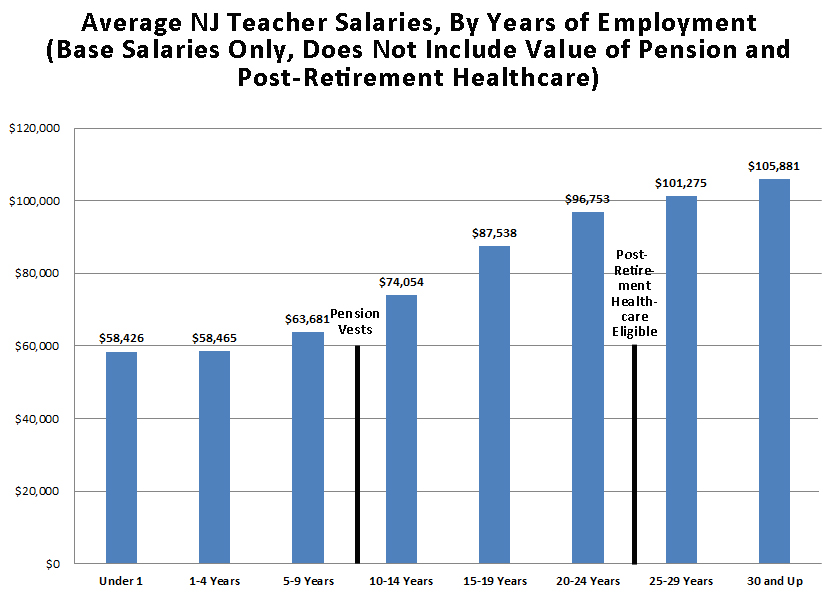

Since New Jersey's average teacher salary is $79,906, versus the $64,545 national salary, New Jersey teacher pensions are substantially higher.

- 1.67% of $79,906 equates to $1334 per year of teaching.

- 1.81% of $64,545 equates to $1168 per year of teaching.

New Jersey's pensions are also based on end-career salaries, which are substantially higher than average salaries. According to the TPAF Valuation Report.

Post Retirement Healthcare

The NJPP/Herzenberg also left Post-Retirement Healthcare out of their reports, even though $1 billion annual expense made by the state for retired teachers.

The NJPP/Herzenberg also left Post-Retirement Healthcare out of their reports, even though $1 billion annual expense made by the state for retired teachers.

Comparing post-retirement healthcare across states is complex and Chapter 78 changed NJ's system to be somewhat less generous to more recent retirees. Data on post-retirement healthcare generosity is difficult to find and compare, but New Jersey's benefits appear to be more generous than in most other states for individual retirees.

A 2016 Pew Report "How States Provide Health Benefits to Retired Workers" sheds light on this elusive subject. Idaho does not offer any coverage. In eleven states all that retired teachers can do is buy into the insurance pool, without any state subsidy. In most other states, the state's subsidy is capped at a certain dollar amount or at a certain percentage. NJ's coverage before Chapter 78 was 100% of costs.

Note: New Jersey's post-retirement healthcare was only created in 1987 and is an underdiscussed cause of the pension underfunding that began in the 1990s. Originally, post-retirement healthcare was paid by a surplus in TPAF and was part of the state's Actuarially Recommended pension payment, but New Jersey abandoned any pretense of pre-funding in the mid-1990s. Since then, New Jersey's post-retirement healthcare has been PAYGO.

Although this was irresponsible of New Jersey, post-retirement healthcare is PAYGO in most states.

Although NJ teachers must work 25 years to receive any post-retirement healthcare (80% of people who ever teach will never receive this benefit), it is also a large expense, $1.0 billion for FY2020, or 6.3% of the all-in the State government's education spending. Post-2011 retirees pay a percentage of health benefits cost.

NJ Pensions Are Tax-Free

Additionally, taxes have to be factored in, since some states claw back some of their pensions in the form of income taxes.

Since 2016's Transportation Trust Fund deal, NJ's pension income has been tax-free: up to $100,000 for married couples, $75,000 for individuals, and $50,000 for married couples filing separately. NJ's exemption thresholds are high enough to exempt nearly all teacher pensions in New Jersey. In most other states pension income is either fully taxable or the exemption threshold is much lower than what it is in New Jersey.

In several of the pension funds that Herzenberg and the NJPP rank higher than New Jersey (California and Massachusetts), pensions are fully taxable.

In New York and Connecticut the exemptions are substantially lower than in New Jersey.

The state income taxes that retirees would pay aren't as large as post-retirement healthcare and Social Security, but they aren't trivial either. For a New York retiree with a $50,000 annual pension, state income taxes are $1,079, even after the $20,000 exemption. The $1,079 is 1.3% of the average teacher's salary.

The state income taxes that retirees would pay aren't as large as post-retirement healthcare and Social Security, but they aren't trivial either. For a New York retiree with a $50,000 annual pension, state income taxes are $1,079, even after the $20,000 exemption. The $1,079 is 1.3% of the average teacher's salary.

In California a retiree with a $50,000 annual pension, state income taxes are $1,563, which is 1.8% of the average teacher's salary.

In New Jersey, a retiree with a $50,000 annual pension would pay $0 in state income taxes on that pension.

Not All COLAs Are Equal

Herzenberg and the NJPP are correct that the lack of a COLA in New Jersey is something that diminishes the value of a New Jersey pension over time, but they lump all states offering COLAs together, even though, COLAs vary considerably from state to state. In many states the COLA is just a partial protection against inflation.

At an extreme of generosity is Illinois, where public workers have a minimum 3% compounding COLA based on the full pension of a retiree, but other states, the COLA is based on a small fraction of the pension and/or don't make the full inflationary increase.

Herzenberg does qualify his championing of other states' COLAs by saying "69 of the 100 largest plans offer retirees some inflation protection" [my emphasis], but he does not say that for many COLA is not fully equal to inflation.

In Massachusetts, the COLA only applies to the first $13,000 of the pension, although it is the full CPI. For the FY2020 budget, the COLA was a maximum of $390.

In California, the COLA is 2%, but it is not compounded, so it is +2% of a retiree's initial pension. Also, the legislature and governor have the power to cancel the COLA if they decide fiscal conditions require it.

California's ad hoc COLA is not unusual. In many states the COLA is granted by the legislature or pension board and can be suspended.

Conclusion

NJ's pensions are but one part of a comprehensive system of benefits for retirees. Saying that NJ's pensions are "among the least generous" in the United States is untrue, because pensions aren't the only benefit retirees get, and those pensions are calculated off of high-salaries and are tax-free.

It's also another reason the NJPP's claims to be a "think tank" shouldn't be taken seriously. It's a PR firm.

It's bad enough that the NJPP/Herzenberg produce highly misleading research and that teachers like Mark Weber and Brian Rock uncritically parrot it, but so do some sources that purport to be more objective.

EG, the Star-Ledger uncritically agreed NJ's teacher pensions were "stingy":

Of the 100 largest public pension plans in the country, we rank 95th, according to a careful study by New Jersey Policy Perspective, a liberal think-tank with the motto "Facts Matter."The acceptance of such biased research as accurate calls into light the NJ media's failure to find disinterested, objective opinions.

The study found that the average pension benefit for public workers is $26,000. The formula used to calculate those benefits is among the stingiest in the nation.

Keep in mind, too, that the bipartisan 2011 pension reform signed by Gov. Chris Christie eliminated cost-of-living adjustments, even for current retirees. So in each year of retirement, public workers see their real pension income drop.

-----

See Also:

- "Can New Jersey Increase Teacher Salaries? Should it? A response to Mark Weber and the NJPP"

- "The Economy and Abbott: What the NJPP Missed in the NJ's Fiscal Disaster"

No comments:

Post a Comment