On Monday, April 29th, the Jersey City Board of Education announced that it was suing the State of New Jersey in order to cancel the redistribution of Jersey City's Adjustment Aid and, apparently, to challenge the constitutionality of SFRA itself.

The lawsuit is being litigated by a Newark law firm called Angelo & Burns. The lawsuit uses data compiled by the Education Law Center, although the ELC itself is not mentioned at all. Based on the press conference, the lawsuit is supported by the Jersey City Education Association.

The core of the Jersey City Board of Education's argument is that the Jersey City Public Schools are below Adequacy and that it is the state's obligation to fund Jersey City at its Adequacy Budget,"From the 2009-2010 school year through the 2018-19 school year, JCBOE has been funded at a cumulative level more than $574,772,516 below that which was necessary for it to provide a thorough and efficient education."

Since Jersey City is below Adequacy and is an Abbott district, therefore it is unconstitutional for the Jersey City Public Schools to lose any state aid.

Page after page of the filing shows that Jersey City Public Schools are below legal Adequacy and "underfunded," although that fact is not in dispute.

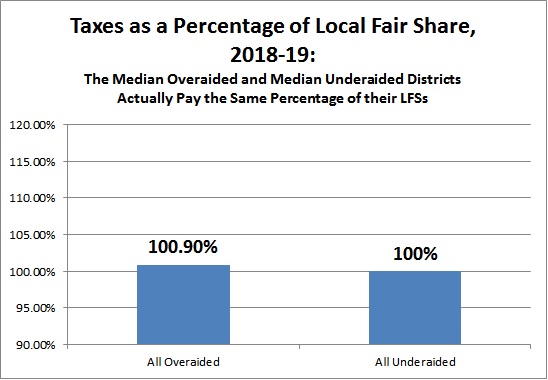

EG:

There are several major problems with the Jersey City lawsuit, the two major ones being:

- S2 eliminated the Tax Cap for Abbott Districts.

- Jersey City does not have municipal overburden.

There is No Tax Cap for Abbott Districts

The lawsuit makes repeated references to the tax cap constraining the Jersey City Board of Education's ability to increase taxes, but what the Jersey City Board of Education doesn't want the public, journalists, judges, or politicians to know is that S2 abolished the tax cap for Abbott districts.

(3) In the case of an SDA district, as defined puruant to section 3 of P.L.2000, C.72 (C.18A:7G-3), in which the prebudget year adjusted tax levy is less than the school district's prebudget year local share as calculated pursuant to section 10 of P.L.2007, C.260 (C.18A:7F-52), the allowable adjustment for increases to raise a tax levy that does not exceed the school district's local share shall equal the difference between the prebudget year adjusted tax levy and the prebudget year local share.Since Jersey City's 2018-19 Local Fair Share was $399 million and its tax levy was $124 million, the Jersey City Board of Education could easily raise taxes by $30 million, $40 million, or $50 million to compensate for the loss of $27 million in Adjustment Aid and to close the deficit with its Adequacy Budget. Legally speaking, the Jersey City Board of Education could raise taxes by $275 million.

The only acknowledgement by the JCBOE that the tax cap was eliminated for Abbotts came in the three words buried here. "SFRA's two percent property tax cap [sic], only recently removed, has constrained the speed with which JCBOE can increase its local revenue to provide funding consistent with its LFS."

There is No Municipal Overburden in Jersey City

Jersey City's school tax rate for 2018-19 was only 0.4241, which is well below NJ's 1.25 school tax rate average, and down from 0.6065 as recently as 2013-14.

|

| Add caption |

In conclusion, the above are just the two major factual and contextual problems with the Jersey City state aid lawsuit. However, he foundational problem with the Jersey City Board of Education lawsuit is that it ignores NJ's fiscal crisis and how the continuation of Jersey City's Adjustment Aid would mean that other districts receive less than SFRA calls for them to get.

-----

See Also:

- "Yes Education Law Center, Jersey City is Ridiculously Overaided"

- "The Abbotts Didn't and Don't Have NJ's Worst Municipal Overburden"