(Adjustment Aid is aid districts get that is above what they economically and demographically need. It is legalized aid hoarding and is unacceptable when there are 118 districts in NJ that get 50% or less of what SFRA recommends.)

The ELC appears to begrudingly accept some redistribution since the statement asks the state to not cut aid for Adjustment Aid districts that are below Adequacy but says nothing about maintaining aid levels for Adjustment Aid districts that are above Adequacy.

From time to time, New Jersey lawmakers raise the prospect of altering the school funding formula by reducing hold harmless aid – called “adjustment aid” in the formula – in some districts and “redistributing” that aid to other underfunded districts. These proposals are a reaction to Governor Chris Christie’s continuing refusal to fund the state aid increases required by the School Funding Reform Act (SFRA), the landmark weighted student funding formula enacted by the Legislature on a bipartisan basis in 2008.

“Districts across the state are experiencing the negative impact of Governor Christie’s decision to chronically underfund the SFRA formula,” said David Sciarra, Education Law Center Executive Director. “However, in the rush to find ‘dollars’ for our public schools, we urge lawmakers not to cut adjustment aid from those districts currently spending below their SFRA ’adequacy budget’.” [my emphasis]

Although the ELC puts the words redistributing and dollars in quotes, like they are too disgusting to utter, this is a softening of their earlier stance against any redistribution. As welcome as this is, their new stance is still highly limiting of the amount of money that would be freed up and would create a set of unfair unintended consequences for high-tax districts and perverse incentives for low-tax districts.

Accompanying its statement on Adjustment Aid, the Education Law Center provides a list of districts getting Adjustment Aid, where districts are grouped according to being above Adequacy or below Adequacy. According to the ELC, there are 71 below Adequacy districts getting Adjustment Aid and 106 above Adequacy districts getting Adjustment Aid.

- The above Adequacy Adjustment Aid districts get $174,024,179 in Adjustment Aid.

- The below Adequacy Adjustment Aid districts get $381,745,553 in Adjustment Aid.

In an $8 billion K-12 aid distribution, Adjustment Aid going to above Adequacy districts is barely 2% of the total. This is not enough to help many of NJ's neediest districts.

Thus, the ELC's redistribution scenario presents a practical problem in that it does not free up nearly enough aid for desperately underaided and desperately below Adequacy districts.

Thus, the ELC's redistribution scenario presents a practical problem in that it does not free up nearly enough aid for desperately underaided and desperately below Adequacy districts.

If the only Adjustment Aid districts that the ELC would accept aid cuts to are above Adequacy, then there is only $174 million theoretically available (and surely these districts wouldn't lose all of that in one year.)

Redistributing part of the $174 million is better than nothing, but it wouldn't be enough to help NJ's most underaided districts.

And even more limiting is the fact that many of the Adjustment Aid districts that are above Adequacy undertax and therefore their surplus about Adequacy is less than the Adjustment Aid they get. For instance, even though Pemberton gets $32 million in Adjustment Aid, it is only above Adequacy by $14 million.

This means that their Adjustment Aid amount is greater than the amount of spending they have above Adequacy. and thus could not lose all of their Adjustment Aid if they are to stay above Adequacy.

HOWEVER, due to undertaxing by above-Adequacy Adjustment Aid districts, the amount of Adjustment Aid available to redistribute is reduced by $80,968,203 ($80,968,203 = $125.6 million - $44.7 million), so from $174 million to only $93 million.

This means that their Adjustment Aid amount is greater than the amount of spending they have above Adequacy. and thus could not lose all of their Adjustment Aid if they are to stay above Adequacy.

| District | (Nominal) Amount of Adjustment Aid 2015-16 | Spending Above Adequacy |

| Asbury Park | $24,422,872 | $13,901,975 |

| Beverly City | $863,310 | $213,799 |

| Gibbsboro | $377,509 | $354,622 |

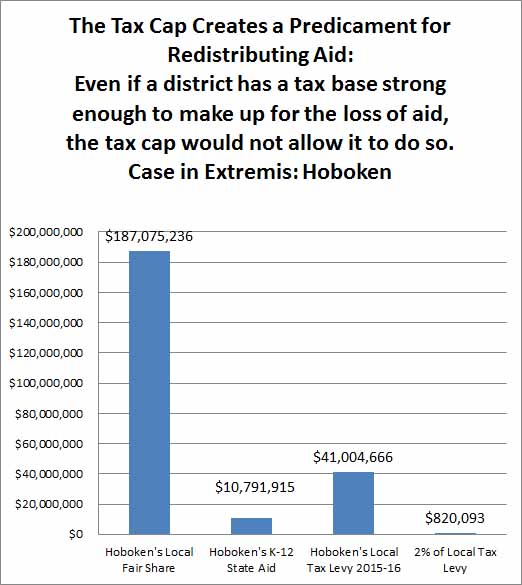

| Hoboken | $5,392,689 | $1,115,016 |

| KeansburgBoro | $8,642,285 | $5,934,890 |

| Lower Cape MayReg. | $6,528,185 | $2,116,251 |

| Manchester Twp | $1,531,444 | $963,844 |

| Middletown Twp | $6,694,364 | $715,837 |

| Morris School District | $252,972 | $50,052 |

| Mount Holly | $1,059,003 | $488,442 |

| Ocean Twp (Ocean) | $5,948,204 | $1,889,703 |

| Ogdensburg | $471,185 | $128,579 |

| Pemberton Twp | $32,419,492 | $14,286,373 |

| Phillipsburg | $9,997,105 | $125,674 |

| Pleasantville | $14,090,235 | $121,805 |

| Tinton Falls | $1,596,766 | $1,043,779 |

| Union Beach | $73,023 | $7,079 |

| Washington Twp (Burlington) | $283,400 | $103,281 |

| West Morris Reg. | $695,639 | $651,903 |

| Wildwood City | $3,567,304 | $87,993 |

| Woodbine Boro | $761,240 | $399,126 |

| $125,668,226 | $44,700,023 |

The ten most underaided districts alone (Manchester Reg, Bound Brook, East Newark, Fairview, Freehold Boro, Guttenberg, Manville, Lodi, North Plainfield, Haledon) have a combined deficit of $91 million.

The amount to take all 50 districts in NJ with greater than a $4,000 per student up to a $4,000 per student deficit (which is still terrible) is $137 million.

The ELC's stance is also a philosophical problem because it rewards districts for not accepting their fair tax burdens and rewards districts for shirking their tax duties. For instance, Jersey City would be exempt from cuts under the ELC's stance, even though Jersey City only pays a third of its Local Fair Share. Toms River would be exempt as well even though it pays 65% of its LFS.

Even Allenhurst, an ultra-ultra-high resource non-operating district that pays less than 1% of LFS, would not lose aid under the ELC's preferred scenario.

The ELC correctly cites the tax cap as a problem because it prevents districts from raising taxes to reach their Local Fair Share. This is a problem, even though Jersey City taxes $225 million below Local Fair Share, at its $114 million tax levy the most it can increase taxes in a year is $2.8 million.

However, the ELC does not call for a waiver for sub-Local Fair Share districts like it called for one for Newark.

The ELC correctly cites the tax cap as a problem because it prevents districts from raising taxes to reach their Local Fair Share. This is a problem, even though Jersey City taxes $225 million below Local Fair Share, at its $114 million tax levy the most it can increase taxes in a year is $2.8 million.

However, the ELC does not call for a waiver for sub-Local Fair Share districts like it called for one for Newark.

- "Increase the City of Newark’s local contribution, utilizing waivers of the 2% annual property tax cap;"

- Is inaccurate by omission because it does not recognize that these districts are under Adequacy because of their own taxes being too low, not because the state isn't giving them enough money.

Also, by focusing on Adequacy there is no chance at all for more aid for an underaided but above Adequacy districts (like West Orange, which accepts an awful tax rate to stay above Adequacy) to get more aid.

If below Adequacy Adjustment Aid districts are shielded from cuts, then they are rewarded for not paying their fair share for their schools.

And yet this is exactly what the ELC calls for:

To take one example: the Toms River Regional School District in Ocean County currently spends $43.7 million below the district’s SFRA adequacy budget. Under the 2% cap, the district could raise only $2.7 million more from local residents. The district receives $11.8 million in adjustment aid. It’s clear from these figures that adjustment aid is a crucial component in the Toms River school budget, as administrators and staff struggle to provide students with an adequate education.

Cutting adjustment aid in Toms River, Middle Township, Jersey City, Atlantic City and other districts spending below their SFRA budgets would lower spending even more and trigger cuts to teachers, programs and services needed for a thorough and efficient education.

Again, many of the below Adequacy Adjustment Aid districts tax significantly below their Local Fair Shares and can economically pay more than they are currently.

Why does the ELC miss this opportunity to call for a tax cap waiver? Districts like Overaided districts like Toms River and Jersey City are going to need these waivers eventually anyway since their tax levies cannot keep up with budget growth and they are not entitled to more aid.

Why does the ELC miss this opportunity to call for a tax cap waiver? Districts like Overaided districts like Toms River and Jersey City are going to need these waivers eventually anyway since their tax levies cannot keep up with budget growth and they are not entitled to more aid.

Finally, it should be noted that the ELC uses the nominal amounts of Adjustment Aid given for 2015-16, even though these figures for Adjustment Aid are badly out of date and would not be the amounts districts would get if the SFRA formula were properly run.

This use of the out-of-date Adjustment Aid amounts significant because there are districts that get money labeled "Adjustment Aid" but who are actually underaided and whose Adjustment Aid should be converted into other streams of aid. For instance Atlantic City receives $7.8 million labeled as "Adjustment Aid," but that Adjustment Aid is a relic of when Atlantic City had a high Equalized Valuation. As for 2015-16, Atlantic City is badly underaided by $31.6 million and that Adjustment Aid should become Equalization Aid.

This use of the out-of-date Adjustment Aid amounts significant because there are districts that get money labeled "Adjustment Aid" but who are actually underaided and whose Adjustment Aid should be converted into other streams of aid. For instance Atlantic City receives $7.8 million labeled as "Adjustment Aid," but that Adjustment Aid is a relic of when Atlantic City had a high Equalized Valuation. As for 2015-16, Atlantic City is badly underaided by $31.6 million and that Adjustment Aid should become Equalization Aid.

Newark is another example; it gets $13 million in money labeled "Adjustment Aid," but is actually underaided by $131.6 million. Likewise with Trenton; which gets $21 million labeled "Adjustment Aid," but is actually underaided by $30 million.

No informed person want Atlantic City to lose aid. Atlantic City's Adjustment Aid is fake and the ELC knows it, so is the ELC bringing them up the prospect of Atlantic City losing aid to scare people away from even considering cutting Adjustment Aid?

Overall, the ELC's new stance is equivalent to a cry "No matter what you do, don't make Toms River and Jersey City raise their taxes!"

Again, I feel the fairest means of redistribution is simply to use actual aid versus uncapped aid and to grant a tax waiver to districts that are taxing below Local Fair Share.